Introduction

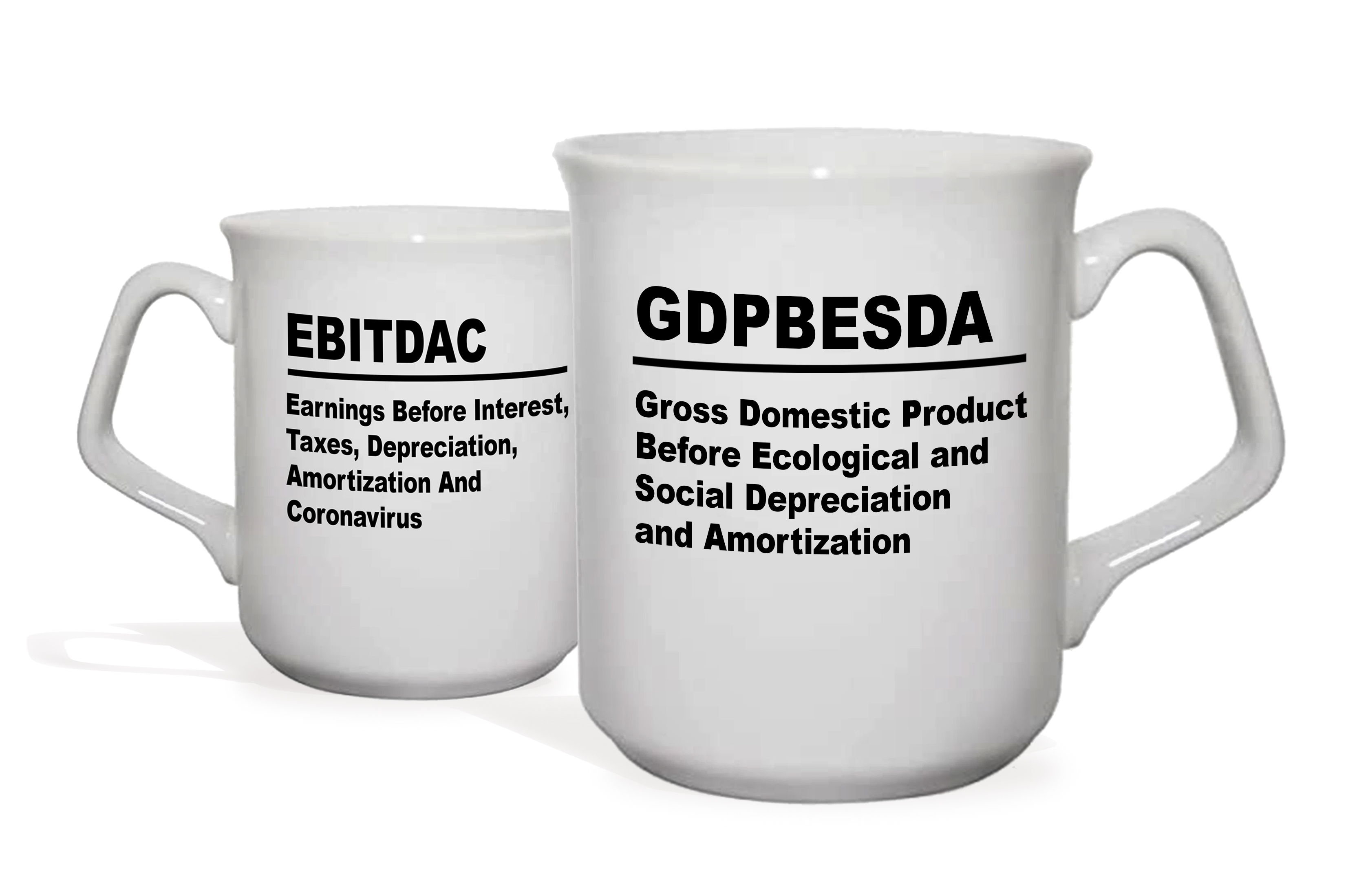

EBITDAC! Brilliant, really. One of a million memes launched by the coronavirus pandemic.

It stands for Earnings Before Interest, Taxes, Depreciation, Amortization and Coronavirus.

It’s a joke.

It’s a play on the discredited EBITDA metric corporations sometimes use to exaggerate their profits – or ‘earnings’ – by excluding as many costs as they think they can get away with and hoping their investment audience will buy the illusion. ‘Don’t focus on our overall Earnings. No, focus on our Earnings before we subtract costs of Interest, Taxes, Depreciation and Amortization.’ And now, also, before costs associated with the coronavirus pandemic.

There is no magician’s sleight of hand involved – EBITDA spells out exactly what they are doing. Instead, it is more the brazen work of the con artist inducing his audience to see just what he wants them to see. EBITDA requires confident presentation to pull off, but also an impressionable crowd to make stick. Yet, there seems no shortage of people willing to believe, so EBITDA persists as an idea. It glows on every Reuters and Bloomberg screen. As Anacharsis of Sycthia archly noted in 580BC1 Geoffrey M. Hodgson, Conceptualizing Capitalism: Institutions, Evolution, Future (University of Chicago Press, 2015). Page 128. :

‘The market is a place set apart where men may deceive one another.’

And, two and a half thousand years later, still we turn up in droves.

Ideas Find People

I searched to see who came up with EBITDAC first, but it appears to be an idea that spontaneously occurred to lots of people at about the same time in late March. Photoshopped mugs suddenly sprouted on social media. (Who does these things so quickly?)

In its trivial way, EBITDAC is an instance of ‘multiple independent discovery’ typical of human scientific and technological advance. It transpires that lots of our conceptual breakthroughs – from the theory of evolution to The Facebook – have occurred independently in separate minds at about the same time.[2]

The world seems to evolve in a way that ideas that were inconceivable a short while ago, suddenly become available to human thought. Such new ideas suffuse the air like spring pollen – or viruses, perhaps – and drift into people’s brain cells seeking articulation and replication. As memes. To really spread, ideas must find hosts with suitably prepared minds. Some people are receptive to a new idea, others don’t have the right receptors for it. As Jung said:

‘People don’t have ideas. Ideas have people.’ [3]

…after that idea had settled into his receptive mind.

In January, it would have been impossible to have the idea of EBITDAC. In March, it was an idea that had occurred to many people. The world unfolds. It is to some degree unprestatable.[4] Things that we could never have seen not so long ago are now as clear as day. We are forever responding to the unfolding and, in so doing, forever influencing the subsequent unfolding that occurs. It’s a loop. Ideas beget ideas, leading us ever on. Sometimes we get out in front. Often we lag behind.

Feinting with Numbers

The humour in EBITDAC offers a portal to seeing some other ideas that have swept us along this recent while, but whose harm we have been reluctant to acknowledge. Good humour is often discomforting – a mirror to certain thoughts we may not have the courage to confront head on.

If we laugh at EBITDAC, we laugh, too, at EBITDA and so should we laugh at GDP (Gross Domestic Product) and all the conventional metrics by which we gauge our economy. They are all arbitrary numbers whose significance depends on our collective willingness to buy into the illusion. The problem is that they are all delusions that work until they don’t. We feint with numbers.

The Idea of EBITDA

Consider first how the idea of EBITDA found certain people and why those people, in turn, thought it an idea worth propagating.

It is sufficient just to contemplate the ‘DA’. With the ‘DA’, EBITDA conveys the profitability of a company as if it would never again have to spend a single dollar on keeping its factories, equipment, property and software in good repair and up to date. In other words, EBITDA excludes the cost of maintaining the whole infrastructure upon which a company depends! It’s the homeowner’s fantasy of how wealthy they would be if they never had to fix or maintain anything in their house ever again. Managers who believe EBITDA is a valid measure of profitability spare themselves the bother of setting aside funds today for foreseeable expenditures tomorrow.

EBITDA came to prominence during the leveraged buyout (LBO) boom of the 1980s, in which investors’ ability to raise funds to take control of companies depended on making those companies appear as profitable as possible. As Moody’s recounted in 2000:

‘LBO sponsors and bankers have promoted the use of EBITDA for its obvious image benefits. EBITDA creates the appearance of stronger interest coverage and lower financial leverage.’[5]

As a general rule, beware profit metrics bearing ‘image benefits.’ Forbes was blunter still:

‘EBITDA is essentially a tool that shows what a company would look like if it wasn’t actually that company.’[6]

A useful trick! I can think of quite a few things that would look better if they weren’t actually the thing that they are.

EBITDA is so much a ‘wool-over-your-eyes’ metric that accounting authorities deny it official status. It is a ‘non-GAAP’ disclosure – not a Generally Accepted Accounting Principle. However, its ongoing ubiquity – besides being trivially easy to calculate – is because it masks the fact that a business might be over-leveraged – that it may have borrowed more than it can ever repay. But, as Warren Buffett perceptively notes, the measure persists because of its power not only to deceive others, but also to help deny:

“People who use EBITDA are either trying to con you or they’re conning themselves.”[7]

Sometimes we use numbers to shield ourselves from what we would rather not know.

Honest businesspeople – and homeowners – know how these stories end. Eventually the under-investment in infrastructure catches up with you. The deception only works for as long as you can get away with the under-investment and the factories and software hold up. Buffett’s partner, Charlie Munger, is characteristically more forthright on the whole topic:

‘I think that, every time you see the phrase “EBITDA earnings”, you should substitute the phrase “bullshit earnings.”’[8]

EBITDA Goes Meta

Seasoned investors may chuckle at all this and counter that they are wise to the deception. (‘We don’t use EBITDA…’).

But, here’s the thing: the exact same pattern repeats at the level of the whole economy and yet many fewer people are laughing.

The point is that the whole financial system operates on a ‘before ecological and social depreciation and amortization’ basis. Our principal economic measure, GDP, excludes the costs of maintaining the ecological and social infrastructure upon which the whole economy depends! In steering by GDP, we are effectively managing society and the planet on an EBITDA basis.

In steering by GDP, we are effectively managing society and the planet on an EBITDA basis.

The danger is considerable. A 2014 study found that the Earth’s annual ecosystem services had been depleted by $20 trillion since 1997, during which time conventionally measured GDP had increased by $29 trillion, for a net gain of $9 trillion.[9] In other words, had the ecosystem loss been set against the monetized gain, headline GDP would have grown only about a third as much as we reckoned. And that estimate was for just a subset of environmental damages and devoid of any social considerations.

Just as EBITDA is the means by which a company can disregard its fraying infrastructure, GDP is the means by which we collectively disregard our fraying social and ecological infrastructure. Eventually, the underinvestment catches up with us. The current pandemic provides a timely example. Early estimates of the economic cost – not to mention the human suffering and grief – of COVID-19 were a conservative $3 trillion against the $3 billion that might have been sufficient to prepare against it.[10]

Our BESDA Economy

We might rechristen GDP as GDPBESDA – Gross Domestic Product Before Ecological and Social Depreciation and Amortization. More simply, BESDA captures the notion that our whole priced economy works on the same basis.

So, every single financial metric on the Bloomberg screen is a BESDA metric – profits-BESDA, earnings per share-BESDA, return on capital-BESDA, return on equity-BESDA, etc. EBITDA-BESDA, even! The millions of financial numbers processed daily by our increasingly automated markets – which, in turn, steer our economy and drag our society along behind, ripping up nature in its wake – are all BESDA numbers.

It is not only EBITDA with which we’re ‘conning ourselves’, but every financial number in the book. They all represent different degrees of disembedded value, some of which we have unmasked, some of which we have not.

That we have our social and ecological sustainability challenges is because the entire financial system repeats the problems of the discredited EBITDA metric at the level of the whole economy. This is the conceptual cage humanity has wrapped around its decision-making and from within which the sustainable development movement is frantically, if futilely, banging its head. But, in view of this bind, the widespread belief that ‘win-win’ sustainability strategies may save the day increasingly resembles a wishful thinking that mere good intentions can overcome the unyielding accounting reality that perpetuates our problems.

To extend Munger’s analogy, GDP is “bullshit wealth creation”. That we have been able to enjoy the comforts of its deception without mishap for so long is simply because the measure was introduced against higher levels of social and ecological infrastructure that we haven’t yet completely run down. The under-investment is only now catching up with us.

Maybe a mug can help fix the point.

Measurements Find People, Too

The problem embodied by both EBITDA and GDP is that they represent partial measures of ‘wealth creation’ disembedded from a larger underlying reality. Yet their continued resonance reveals the mysterious power of measurement.

In an age when it is becoming trivially easy to measure almost anything, we are slowly learning the wisdom of not measuring something, lest it lead us on. ‘What gets measured gets managed’, goes the adage. But, eventually, what gets measured manages us. It’s a loop.

What gets measured gets managed…eventually manages us. It’s a loop.

Measurements are partial and performative – partial in necessarily grasping only a small sliver of reality and performative in their strange power to bend human attention and effort to what is measured. So, measurement is always a double-edged sword. It brings something into view only by forcing other things out of sight, much as the human eye summons focus only by giving up peripheral vision. A measurement is always simultaneously a masking. Just because we have the idea to measure does not always make it wise to measure.

Awareness, or not, of this paradox is a deep fault line that has divided interrogators of the world. Physicists have always loved a good measurement. Lord Kelvin, for example:

“When you can measure what you are speaking about, and express it in numbers, you know something about it; but when you cannot measure it, when you cannot express it in numbers, your knowledge is of a meagre and unsatisfactory kind; it may be the beginning of knowledge, but you have scarcely in your thoughts advanced to the stage of science.”

Others have been wary about what the impulse to measure risks leaving behind. Reflecting on what our quantitatively-driven Scientific Revolution has excised from our interpretation of the world, RD Laing offers:

“Out go [qualitative] sight, sound, taste, touch and smell…Experience as such is cast out of the realm of scientific discourse.”[11]

What GDP casts out

Economics and finance – with all their measurements – are two influential vectors by which we have gradually submitted our collective self-management to a quantification that casts out much of human experience. EBITDA is so trivial a measure, its promoters can afford to spell out its excisions and overtly advocate its significance to its narrow audience. Caveat Emptor, and all that. But, with GDP and its many derivatives that guide our collective decision-making at larger scale, we have been less transparent about what is left behind. What is it that looms large when we measure GDP and what do we effectively cast out of the realm of discourse?

GDP is essentially an aggregation of all priced exchanges, so cultures that steer by GDP opt to favour the priced over the unpriced. In turn, this raises a critical question: why do some of the things humans value have prices? And why do some not?

Why do some of the things humans value have prices? And why do some not?

A complicated issue, but the basic answer is that what is priced emerges from the combination of physical accident and haphazard cultural choice.

Physically, certain things of value are easily commodifiable, while others are not. Goats come in discrete units and land can be enclosed, but trust and fresh air resist easy commodification. Atop this feasibility of commodification lies all the haphazard cultural decisions to confer – or not – the property rights that may enable commodifiable things to be owned and exchanged. Beaches are a good example. Any beach can be technically parcelled or enclosed, but cultures differ on whether beaches can be privately owned or not. This piecemeal mix of commodifiability and cultural choice determines the extent to which GDP grasps human experience.

At root, our social and environmental sustainability challenges arise from the fact that our economy prices only some things of value, yet we behave more and more as if our economy prices everything of value. We treat EBITDA as a meme-worthy joke, but we take GDP seriously. It is always easier to identify individual fools than to admit a collective foolishness.

But it matters in a culture which steers more and more by its market signals. Over the last four decades, Western cultures have elevated market institutions over non-market institutions in determining culture’s course. ‘It’s the economy, stupid’, intoned a successful leader of recent times. A central claim supporting this development is that markets are value-neutral – no individual’s preference is imposed upon another.

Yet at a higher level, elevating market outcomes within cultural decision-making smuggles in the meta-value that things that are commodifiable and exchangeable are more valuable than things that are not. Which sounds like some peoples’ preference being imposed upon others. Value-neutrality is another of our illusions.

In a world where prices are incomplete – and can never be complete for technical reasons – the market, which knows only prices, might usefully be counter-balanced by non-market institutions that can uphold the importance – the value – of what cannot be commodified and priced. Of course, this can never be justified by market logic – any more than a blind man can contribute to a debate on colours. It is extra-economic or meta-economic reasoning. It demands recalling what has been masked by the act of economic measurement.

The Body Keeps the Score…

Yet, if we are deeply inclined to measure, as we seem to be, are there better metrics we can find? We might lift up our measures of EBITDA and GDP and see what lies underneath. We might aim for the very heart of things.

Psychiatrist Bessel van der Kolk had an interesting idea – or at least propagated an interesting idea that had him:[12]

‘The body keeps the score.’

His insight from working with mental trauma patients was that even if humans appear outwardly to have overcome traumatic past events, the toll of those events can remain stored in the body in everything from subtle postural tensions to stubborn and problematic behavioural traits. The body has not forgotten past harms even if the mind can occasionally pretend otherwise. The body keeps the real score.

Van der Kolk and fellow therapists argue that real healing and real growth only results from patients confronting the real score maintained by the body, not the more agreeable score the mind might imagine, but whose very imagining requires such self-delusion that its disintegration is only a matter of time.

More generally, the body keeps the score for all of us, not just those who have suffered unusual harms. In its daily juggling of internal biochemistry, the body increases or decreases various mood-governing substances – cortisol, serotonin, dopamine and more. In a sense, these chemicals are the currencies that really matter. Their relative levels – their ‘exchange rates’ almost – determine whether we are joyful or sad, relaxed or stressed, open or closed. Their levels are important both in the moment and in their continual shaping of our bodies to influence the dispositions we carry with us into the future.

We try and manipulate these internal currencies via medicines, but with limited success. To the frustration of doctors, certain medicines that promise in theory to alleviate mental suffering fail because they are either partially or wholly repelled by our protective blood-brain barrier. Alas, they cannot get to where they might be helpful. Sustainable happiness cannot simply be ingested. This is a real-life capital controls problem – ‘wealth’ in one location cannot be transformed into ‘wealth’ in another location. Worse still, efforts to force the issue can sometimes backfire to create adverse side-effects.

In a similar way, there is something akin to a bank account-body barrier where what we track and accumulate as external wealth cannot fully cross over into the body and affect the bodily scores that really matter. Certainly, there is meaningful absorption at lower doses. Initial increments of monetary wealth reliably have a significant positive effect on quality of life. But, as the trajectory of more developed countries has shown, the body’s capacity to convert higher levels of wealth into sustainable happiness starts to approach saturation. Diminishing marginal returns creep in. Worse, beyond a certain point, pursuing measured wealth risks serious side-effects.

… And The Earth Keeps the Score

Analogously, and at the very bottom of things, the Earth keeps the real score of our overall economy. Its ecosystems bear the marks and scars of our past actions and behaviours. Some of our piecemeal measures are beginning to grasp the comprehensive systemic harm we cause.

We have ‘severely altered’ 75 percent of terrestrial ecosystems. Possibly more remarkable, given that we are land-based mammals, we have similarly altered 66 percent of marine ecosystems. An eighth of extant species are currently threatened with extinction. Eighty-five percent of the wetlands present in 1700 have gone. Half of coral reefs have died since the 1870s.[13]

The Earth’s lungs are compromised. An area of forest the size of the UK is being lost every year – a respiratory problem of global scale.[14] We have discerned that the Earth is running a slight temperature, yet by emitting 36 billion tons of CO2 to the atmosphere in the last year we seem keen to induce a full fever.[15]

These few indicators suggest that the Earth keeps a very different score to the one our economic and financial metrics display. It appears there is a profound economy-earth barrier where not only can our economic wealth not cross over and benefit the Earth, its accretion is now coming at the Earth’s expense. And so, in time, at our own.

One of the profound impacts of COVID-19 is its forcible reminder of our animal selves. Modern technology has beckoned us towards a virtual world and to a collective experience that is increasingly ‘out of body’. Networked together by the Web, we were newly enamoured by a sense of being a hive mind. COVID-19 has abruptly reminded us that while we may be hive mind, we are also herd body, utterly dependent upon Earthly processes. Our escape into the virtual has been thwarted.

We are hive mind and herd body. Utterly dependent upon Earthly processes.

The hive mind can trick itself for a while. Temporarily, if enough people believe, even very disembedded measures of wealth can become self-fulfilling frames on the world, capable of influencing the unfolding that subsequently occurs. Indeed, for a time, they may even be functional or beneficial delusions – shared ‘imagined orders’ around which we can self-organize, be productive and achieve considerable feats.

But, all the while, Planet Earth keeps track of the real score. The score may sometimes disappear from view but it cannot be indefinitely suppressed. It, will, in time, intrude back into our perceptions and remind us of reality. The delusions will fall away.

Real growth only ever comes from confronting the real score.

*

*

References

[1] Geoffrey M. Hodgson, Conceptualizing Capitalism: Institutions, Evolution, Future (University of Chicago Press, 2015). Page 128.

[2] See https://en.wikipedia.org/wiki/List_of_multiple_discoveries for a long list.

[3] As cited by Jordan Peterson. Dostoevsky seems to have inhaled the idea even earlier in his 1872 novel Demons: ‘It was not you who ate the idea, but the idea that ate you.’

[4] Unprestatable is a term coined by biologist, Stuart Kauffmann, to capture the idea that the emergence of life is continually unfolding into a ‘fog of the unknowable’. The intrinsically combinatorial nature of biological, technological and intellectual development means that there are some future combinations of ideas and events that will arise from combinations of things we can only barely discern today. Wonderfully, the word seems not to have existed before he first stated it.

[5] Pamela M. Stumpp and others, ‘Putting EBITDA In Perspective Ten Critical Failings Of EBITDA As The Principal Determinant Of Cash Flow’ (Moodys Investor Services, 2000).

[6] Ted Gavin, ‘Top Five Reasons Why EBITDA Is A Great Big Lie’, Forbes, 2011 <https://www.forbes.com/sites/tedgavin/2011/12/28/top-five-reasons-why-ebitda-is-a-great-big-lie/>

[7] http://buffettfaq.com/#your-thoughts-on-ebitda

[8] http://buffettfaq.com/#what-adjustments-to-reported-earnings-do-you-make

[9] Robert Costanza and others, ‘Changes in the Global Value of Ecosystem Services’, Global Environmental Change, 26 (2014), 152–58 <https://doi.org/10.1016/j.gloenvcha.2014.04.002>.

[10] Akshat Rathi, ‘What Links Coronavirus and Climate Change: Lack of Preparation’, Bloomberg.Com, 7 April 2020 <https://www.bloomberg.com/news/articles/2020-04-07/what-links-coronavirus-and-climate-change-lack-of-preparation>

[11] RD Laing quoted in Fritjof Capra and Pier Luigi Luisi, The Systems View of Life: A Unifying Vision (Cambridge University Press, 2014).

[12] Bessel van der Kolk, The Body Keeps the Score: Mind, Brain and Body in the Transformation of Trauma (Penguin UK, 2014).

[13] IPBES Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services, Summary for Policymakers of the Global Assessment Report on Biodiversity and Ecosystem Services (Zenodo, 25 November 2019) <https://doi.org/10.5281/zenodo.3553579>.

[14] Fiona Harvey, ‘World Losing Area of Forest the Size of the UK Each Year, Report Finds’, The Guardian, 12 September 2019, section Environment <https://www.theguardian.com/environment/2019/sep/12/deforestation-world-losing-area-forest-size-of-uk-each-year-report-finds>

[15] Zeke Hausfather, ‘Analysis: Global Fossil-Fuel Emissions up 0.6% in 2019 Due to China’, Carbon Brief, 2019 <https://www.carbonbrief.org/analysis-global-fossil-fuel-emissions-up-zero-point-six-per-cent-in-2019-due-to-china>

.

Leave a Reply